In January 2026, Macquarie Bank hit 99.98% system availability. The same month, one of the Big Four experienced a multi-hour outage that locked customers out of their accounts.

This is not a coincidence. It is the result of decisions made years ago about infrastructure, culture, and what kind of company a bank should be.

Macquarie runs 97% of its workloads on public cloud. It rolled out Google’s Gemini Enterprise AI platform to every retail banking employee—not just the tech team. It launched Q, an AI agent that handles customer queries around the clock. And it did all of this while maintaining the kind of reliability metrics that most legacy institutions treat as aspirational.

The comparison is instructive. Not because every organisation should copy Macquarie’s playbook, but because the principles underneath translate to any industry grappling with digital transformation.

The Digital-First Foundation

In 2022, Macquarie became the first Australian bank of size to run its core banking platform on public cloud. This was not a lift-and-shift migration. It was a fundamental redesign of how the bank operates.

The results show up in customer experience. Account opening takes minutes, not days. New customers can have their identity verified, account created, and debit card loaded into Apple Pay or Google Wallet in a single session. No branch visit. No waiting for a physical card in the mail.

“Retail banking is a highly competitive industry, and ultimately we need to scale fast and scale smartly,” says Richard Heeley, Head of Technology at Macquarie’s Banking and Financial Services group.

The cloud foundation enabled everything that followed. Real-time processing. Rapid feature deployment. The infrastructure to support AI at scale.

The AI Acceleration

By April 2025, Macquarie had more than 30 AI-augmented products and services in development. By October, they had rolled out Gemini Enterprise to every employee in their retail banking business.

This is unusual. Most enterprises limit AI tools to technology teams or run small pilots. Macquarie took a different approach: democratise access and let the organisation figure out where AI creates value.

“If an AI initiative doesn’t result in better features, a more seamless customer experience, or more reliable service for our customers, we question its value,” says Ashwin Sinha, Chief Data, Digital and AI Officer at Macquarie Bank. “Everything comes back to creating happier customers who want to engage with us more.”

Within six months of rollout, Macquarie targeted having all employees incorporating AI into their daily workflows. Ninety-nine percent of employees completed generative AI training.

The bank is building two types of custom agents: personal agents for individual productivity and enterprise agents designed to address complex business challenges like fraud detection, where AI now reduces false positive alerts by 40% and directs 38% more users toward self-service.

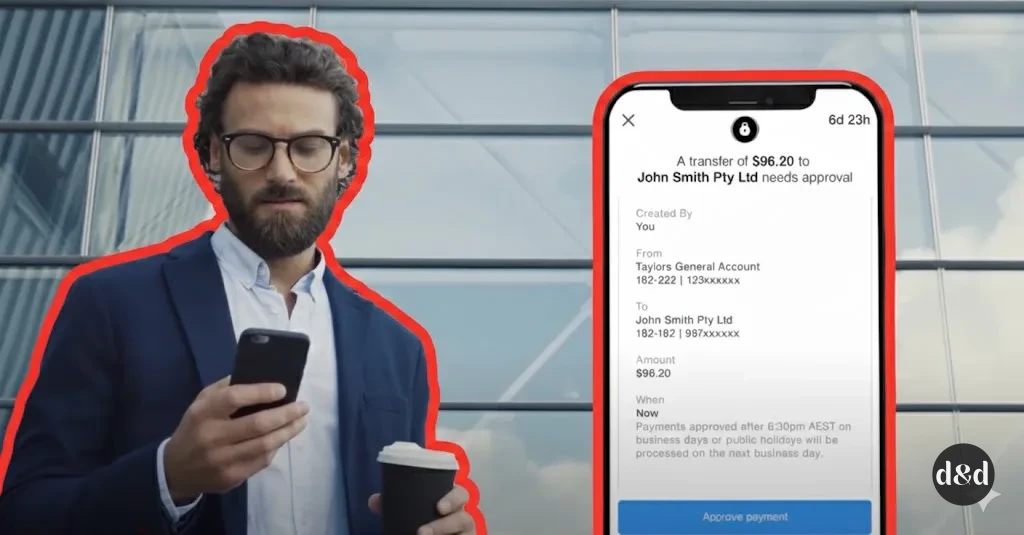

Q: The Customer-Facing AI Agent

In January 2026, Macquarie launched Q—an AI agent available through the mobile banking app and online banking site. It uses natural language processing to handle customer queries about services and accounts, available around the clock.

Q is not a chatbot in the traditional sense. It is built on what Macquarie calls “Macquarie Intelligence”—the combined knowledge and expertise of the bank’s people integrated with advanced AI. It uses two-factor authentication for security and encryption to protect customer data.

“Q is designed to evolve quickly as more people use it,” Sinha says. The bank will expand capabilities based on real customer feedback.

Macquarie vs The Big Four: The Comparison

The gap between Macquarie and the traditional Big Four (Commonwealth Bank, NAB, ANZ, Westpac) is not about resources. It is about architecture, culture, and willingness to move.

| Factor | Macquarie Bank | Big Four Banks |

|---|---|---|

| Cloud Infrastructure | 97% public cloud | Hybrid systems, legacy core platforms |

| AI Deployment | Gemini Enterprise to all employees | Siloed pilots, primarily tech teams |

| Account Opening | Minutes (fully digital, instant card) | Often requires branch visit or days wait |

| Open Banking | First in Australia to launch platform | Reactive, compliance-driven adoption |

| Customer AI Agent | Q (launched Jan 2026, 24/7) | Basic chatbots, limited capability |

| System Availability | 99.98% (2026) | Periodic major outages |

| Critical Incidents | 59% reduction achieved | Ongoing reliability challenges |

The Big Four are not standing still. Westpac recently unveiled its “Intelligence Layer” platform. Commonwealth Bank has invested heavily in AI. But the starting point matters. Migrating decades of legacy infrastructure while maintaining daily operations is fundamentally harder than building cloud-native from a cleaner base.

What Macquarie Gets Right

Three principles stand out from Macquarie’s approach:

Customer lens on technology decisions. Every AI initiative gets evaluated against customer impact. This is not a platitude—it is a filter that kills projects that might be technically interesting but do not create customer value.

Full organisational rollout, not pilots. By giving every employee access to AI tools and training, Macquarie discovers use cases that central teams would never imagine. The innovation comes from the edges, not just the technology department.

Reliability as a feature. The bank hired leaders with Google-level site reliability engineering experience and applied those principles to banking. “Tech companies treat their systems like cattle. Banks treat their systems like pets,” says divisional director Vin Grasso-Nguyen. “I had to shift my mindset from herding cattle to looking after pets.”

Five Career Takeaways for Fintech Professionals

Macquarie’s transformation offers lessons that apply beyond banking:

1. Cloud infrastructure is table stakes, not competitive advantage.

The advantage comes from what you build on top. Macquarie’s cloud migration enabled real-time processing, rapid deployment, and AI at scale. The cloud itself is just the foundation.

2. AI democratisation beats AI centralisation.

Restricting AI tools to technical teams limits what you discover. Macquarie’s approach—train everyone, give everyone access, see what emerges—surfaces use cases that centralised planning misses.

3. Customer experience metrics should drive technology decisions.

Macquarie filters every initiative through customer impact. If it does not make customers happier or more engaged, it does not ship. This discipline prevents technology for technology’s sake.

4. Reliability is a competitive moat.

In an industry where outages make headlines, 99.98% availability becomes a brand asset. Customers notice when their bank works when others do not.

5. Legacy institutions can move fast—but architecture determines speed.

The Big Four have more resources than Macquarie. But decades of accumulated technical debt create friction that no amount of budget can immediately solve. For anyone building a career in fintech, understanding the constraints of legacy systems is as important as understanding new technology.

The Broader Lesson

Macquarie’s thesis is straightforward: act like a tech company that happens to do banking, not a bank that happens to use technology.

“We had to become the best tech company in financial services,” says Grasso-Nguyen.

This is not about being anti-tradition. Macquarie still has physical presence, human advisers, and the full regulatory apparatus of a licenced bank. The difference is in how technology decisions get made, how quickly they ship, and how ruthlessly they filter for customer value.

For professionals working in fintech, adjacent industries, or any organisation wrestling with digital transformation, the pattern is worth studying. Not because Macquarie has all the answers, but because they made a bet on digital-first architecture years ago and are now compounding the advantages of that decision.

The Big Four will catch up eventually. But “eventually” can be a long time in a competitive market.

While the Big Four were digitising their existing branch model, Macquarie quietly built a platform-first business that generates higher returns with a fraction of the physical infrastructure. The lesson: digital transformation isn't about making your current model faster. It's about questioning whether the model itself still makes sense.

Key Takeaways

-

97% cloud-native architecture:

Macquarie's public cloud migration enabled real-time processing, rapid deployment, and AI at scale—capabilities legacy systems struggle to match.

-

AI for everyone, not just tech teams:

Rolling out Gemini Enterprise to all employees (99% trained) surfaces use cases that centralised planning misses.

-

Reliability as brand differentiation:

99.98% availability and 59% fewer critical incidents become competitive advantages when competitors make headlines for outages.

-

Customer lens filters everything:

If an AI initiative doesn't create happier customers, it doesn't ship. This discipline prevents technology for technology's sake.

-

Architecture determines speed:

The Big Four have more resources but decades of technical debt. Starting position matters more than budget.

What Macquarie's AI rollout means for everyone else

Macquarie's lead isn't really about AI at all. It's about the unglamorous layer underneath: a cloud-native architecture, clean data, and documentation good enough that a model can point at something specific. That's the foundation most smaller firms are missing.

Generative AI is levelling the playing field faster than most realise. A small practice with good context can now run AI workflows that used to need a team of analysts. The tools are only as good as what they know about your business.

That's what we do at jopy.agency. We audit how your firm actually runs and produce structured files: Operations-Model.md, Brand-Positioning.md, Customer-Journey.md, Tech-Stack-Audit.md (to name a few). They give any LLM real context on your business, without needing a Macquarie-sized program to get there.

What are Structured .md files?

Markdown (.md) is the cleanest and smallest file format that AI likes to read.

We audit businesses end to end, your operations, workflows, brand, customers, tech, etc., then write all of it into structured .md files.

Then you can use these structured .md files so ChatGPT, Claude, Gemini, or any chat-based LLM can read your business context properly for future, in-house vertical growth.

You can then use AI in-house for ops, client comms, internal research, reporting, or whatever lands most value.

Interested in AI Context Auditing? Visit Jopy.agencyInterested in AI Context Auditing?Cite This Article

APA 7THReferences

Formatted in APA 7th Edition

- Saarinen, J. (2026, January 20). Macquarie Bank unveils customer-facing 'Q' AI agent. iTnews. https://www.itnews.com.au/news/macquarie-bank-unveils-customer-facing-q-ai-agent-623042

- Google Cloud. (2025, October 9). Macquarie Bank Democratizes Agentic AI, Scaling Customer Innovation with Gemini Enterprise. Google Cloud Press Corner. https://www.googlecloudpresscorner.com/2025-10-09-Macquarie-Bank-Democratizes-Agentic-AI

- Technology Magazine. (2025, October 9). Inside Google's Comprehensive New Gemini Enterprise Offering. https://technologymagazine.com/news/inside-googles-comprehensive-new-gemini-enterprise-offering

- iTnews. (2026, February). Macquarie brings agentic SRE to its digital bank. https://www.itnews.com.au/news/macquarie-brings-agentic-sre-to-its-digital-bank-623685

- Google Cloud Blog. (2026, January 7). Google Cloud's Business Trends Report 2026: Key findings. https://blog.google/products/google-cloud/ai-business-trends-report-2026/

- Macquarie Group. (2023). Australia's fastest digital account opening experience. https://www.macquarie.com/au/en/insights/australias-fastest-digital-account-opening-experience.html

- Macquarie Bank. (2026). Q AI Agent. https://www.macquarie.com.au/digital-banking/q-ai-agent.html